In most instances, a withdrawal from a 401K prior to 59½ results in the amount being taxed at your income tax rate plus an additional 10% penalty (IRS). This rule is to encourage people to use these funds only for retirement. However, despite what you might think, there are several exceptions to this rule. In this article, we will go over the number of ways to take your money out of your 401k without penalty. We’ll also discuss whether this is something you should even do.

Wait for Retirement

Waiting for retirement is probably the best way to take money out of your 401K without penalty. This approach doesn’t involve you taking any loopholes or risking your chances of having a comfortable retirement. To do this, all you would have to do is allow your savings to sit in your 401K account until you turn 59½. Doing so would allow you to avoid the 10% penalty and reap the tax benefits your 401K offers.

One of the biggest criticisms of 401Ks (and other retirement plans) is that the age of withdrawals (59½) is too old. Many may think: “I don’t want to retire so late. Why should I be living my life to the fullest at such an old age?” While I understand the idea behind this, I also think this isn’t correct. The reason for this age requirement is to ensure younger adults don’t waste their retirement savings. Having this requirement and an early withdrawal penalty makes it so you keep the money in your account until you retire.

Additionally, 59½ is not all that old. According to the CDC, the average lifespan in the US is 76.4 years old. That means, if you retire at 60, you will have over 15 years of retirement as of today. As technology advances, I’d expect this life expectancy to increase, meaning retirements will only become longer. This means your quality of life at an older age will likely not decline as dramatically as it does today.

Again, I do understand the argument. Working for 40 straight years of your life might seem a little overboard. But, choosing not to use a 401K because of the retirement age isn’t a solution.

Roth 401K Contribution Withdrawals

From here on out, all of these methods involve early withdrawals (which is before 59½). The simplest way to take money out of 401k without penalty involves Roth 401K contributions. Roth 401Ks are unique because all contributions are made post-tax. Since they are after-tax funds, all contributions can be withdrawn without tax or penalty (Bankrate). However, you would still have to pay tax on any earnings withdrawn from the account. For example, if you contributed $50 and earned $100 in your 401K, you would be able to withdraw the $50 without penalty but not the $100. The $100 is a gain that would be subject to both the early withdrawal penalty and applicable taxes.

Rule of 55

If you leave your employer in the year you turn 55 or after, you are able to withdraw from that employer’s 401K (or 403(b)) plan without penalty. If you are a public safety worker, you may be able to do so in the year you turn 50. While it is penalty-free, you still have to pay the income tax associated with the withdrawal.

It doesn’t matter why you left your employer either, whether it’s retirement, layoff, quitting, or firing. This doesn’t mean you have to stop working, however. You are able to return to work once leaving this employer.

It’s worth noting that not all employers allow for this early withdrawal and, if they do, they might require the withdrawal to be in a single lump sum. If this is the case, then it could have serious tax consequences. Additionally, this rule only applies to plans of your most recent employer. The IRS does not allow this exception for plans with earlier employers. To use Rule of 55 with those funds, you would need to roll over those accounts into the plan provided by your most recent employer.

This can be very beneficial to those looking to retire early. Social Security benefits are not available to you until you turn 62. So, this can allow you to get a headstart on your retirement without having to pay a penalty (SmartAsset). However, it’s important to keep in mind that these funds should last for the entirety of your retirement. Prematurely touching your retirement funds can be risky.

Substantially Equal Periodic Payments (SEPP) or Rule 72(t)

Under code 72(t), section 2, individuals can make early withdrawals without penalty if they meet certain SEPP requirements. The requirements include having to take at least five ‘SEPPs’ based on a calculation using your life expectancy through one of the IRS-approved methods. You can read more on these methods in this Investopedia article. Also, the withdrawals must follow a specific schedule for 5 years or until you turn 59½, whichever is later.

While this could help those looking to retire early, it also can be dangerous to withdraw from a retirement account at an early age. Investopedia sees this method as a ‘financial last resort,’ as the IRS does allow for other exceptions in case of specific emergencies. Whenever you consider making an early withdrawal, consider how it can impact your retirement.

Hardship Withdrawals

If your employer allows it, you can take money out of your 401K without penalty for “an immediate and heavy financial need” (Bankrate). Hardships include unreimbursed medical expenses, payments necessary to prevent eviction/foreclosure on a principal residence, funeral or burial expenses, purchase of a principal residence, to pay for certain expenses for the repair of damage to a principal residence, and payment of college tuition and related educational costs. While this may sound like a positive, it definitely has drawbacks.

If you decide to do this, the IRS wouldn’t allow you to replace or return these funds back to your account. In other words, once you withdraw these funds, they are permanently removed from the account. You would need to make normal contributions to replenish what you withdrew.

Additionally, your employer may freeze your contributions for several months after this withdrawal. So, doing this could definitely be a setback for your retirement planning. You should only look at hardship withdrawals in cases of extreme financial hardship. Otherwise, you should look to other means, like an emergency fund.

401K Loans

In this scenario, you’re loaning yourself money from your 401K plan. The requirements of the loan may depend on your employer. Some employers may not even offer this as an option. Your employer would lay out whether they offer this in addition to the maximum and minimum amounts and any rules that you need to follow.

Typically, employers allow you to take out as much as 50% of your vested account balance up to $50,000 in a year. It’s also common for employers to allow only one loan at a time and to require consent from a spouse/partner prior to opening one. Additionally, for these loans, you’re required to pay back the principal and interest within 5 years. In other words, you are paying yourself back with interest.

401K Loans vs. Hardship Withdrawals

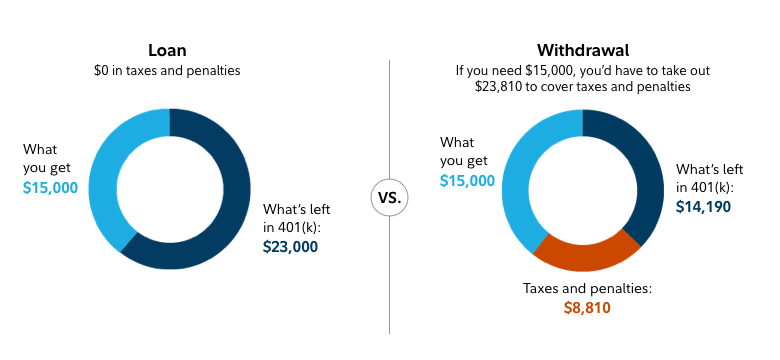

Fidelity makes an argument that a 401K loan can be the preferable option compared to a hardship withdrawal. Let’s take a look at the following example:

Taking a loan: A 401K participant with a $38,000 account balance who borrows $15,000 will have $23,000 left in their account.

Taking a withdrawal: If that same participant takes a hardship withdrawal for $15,000 instead, they would have to take out a total of $23,810 to cover taxes and penalties, leaving only $14,190 in their account.

When taking out a hardship withdrawal, you still owe taxes. So, you would need to take out additional funds from your account to cover the tax expense. With the loan route, however, you do not owe taxes since it is a form of debt that you pay back. This means you’d be able to keep more funds within your 401K.

While a 401K loan might sound interesting, it definitely has its drawbacks. For one, the interest you pay yourself will likely not be greater than the return you’d realize leaving the money in your account. For example, if you pay 3% interest towards your account, that would be lower than the average S&P 500 return of 8% (Official Data Foundation). You are able to make contributions to your 401K with a 401K loan outstanding (Forbes). But, having to pay principal and interest payments may take away from those contributions. This would be harming your retirement savings in an indirect way.

Further, since it is a loan, you do run the risk of defaulting on it. If you are unable to make payments on a 401K loan, it’s basically treated as an early withdrawal. In that case, you would be subject to applicable income taxes and that 10% penalty. Also, if you leave your employer that sponsored the plan without paying off the loan, you’d have a small time window to pay off the loan. So, ‘defaulting’ on the loan is something that can happen.

Other Exceptions:

IRS Levies: If you are required to pay previously unpaid federal taxes, the IRS can withdraw from your IRA penalty-free. In this case, the IRS must be the one making the withdrawal to avoid penalties.

Medical Debts: If you are in debt for medical expenses that are greater than a specific percent of your adjusted gross income, you are able to make a penalty withdrawal in the same year as the expense.

Permanent Disability: If you are permanently disabled and physically unable to work, you can make tax-free withdrawals. These withdrawals can be used for any purpose. However, you may need to show evidence of the disability.

Divorce Settlements: You may make penalty-free withdrawals if it is for payment as part of a divorce settlement/agreement.

Active Military Deployment: If you are a reserve in the military and are called into active duty for at least 179 days, you may make ‘qualified reservist distributions’ without penalty.

Birth or adoption of a child: You are able to withdraw $5,000 within the first year of a child’s birth/adoption without penalty.

Should You Make Early Withdrawals?

Now that you know how to take money out of 401k without penalty, you might be itching to do so. However, that might not be in your best financial interest.

Honestly, in most cases, it doesn’t make sense to touch your retirement savings early. The majority of the exceptions I just listed should only be used as a last resort. Withdrawals from your account would limit the growth potential of your savings. Leaving your money within your 401K will allow it to compound over time, which greatly improves your chances of retiring comfortably. Just because you can take money out of your 401k without penalty doesn’t mean you should.

With proper budgeting and planning, there rarely should be a reason for you to make an early withdrawal. For example, there is no need for a hardship withdrawal if you already have an emergency fund, which would also eliminate the need for the majority of other exceptions listed.

Some looking to retire early (I’m @ing you FIRE Movement) might benefit from the Rule of 55 and Rule 72T. However, before you look to use these options to retire early, please consider consulting a financial planner or professional. Your retirement is not something that you can play around with. Ensure that retiring early is in your realm of possibility before committing to it. Otherwise, you’d be jeopardizing your ability to retire at all.

Regardless, I think it is important to know that they are available. Everyone’s financial situation is unique, and yours might require the use of one of these. So, it’s best to understand what options you have.

To learn everything you need to know about 401K plans, you can read my Ultimate Guide to 401K Plans here!