In a study conducted by the TIAA Institute, American women on average scored ten percentage points worse than their male counterparts on a financial literacy exam. I’d confidently argue that this isn’t the result of inability. Rather, this phenomenon is likely the result of not having access to resources. Regardless, this is an alarming statistic, as being financially illiterate is specifically damaging to women.

In addition to lacking educational resources, women also face unique financial obstacles not faced by men. These hurdles include earning less, independent/longer retirements, and shorter careers. Being even less financially literate than men, women do not have the tools necessary to navigate what’s already a more difficult financial situation.

In this article, we will examine these obstacles in detail to demonstrate their severity and how proper financial education could alleviate the situation.

A Deeper Look at the Literacy Disparity

As mentioned previously, women in the US struggle with financial illiteracy far more than men. It’s worth noting that this issue only appears to be worse in younger women. In that same TIAA study, Gen Z women (the youngest demographic) scored 38%. In contrast, Baby Boomer women (the older demographic), scored 51% on average. This marks a double digit difference in scores, suggesting that this literacy disparity is only worsening in the United States.

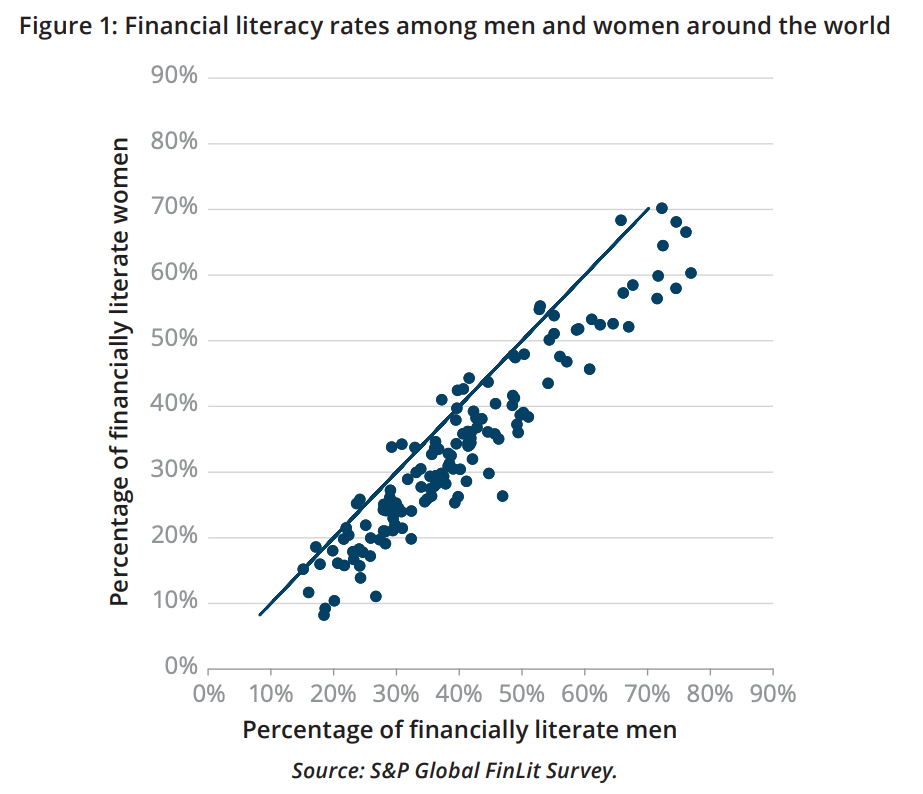

While I’ve only highlighted this issue within the US so far, this is not solely an American issue. Across the globe, women are financially illiterate at higher rates than men. On a global level, roughly 35% of men are financially literate, while only 30% of women are (Hasler and Lusardi). For nations in all stages of development, women fail to grasp even the most basic financial principles at the same rate as men.

It’s interesting to note that such a disparity does not exist when males and females are in their teenage years, according to the OECD. This means that, as these individuals begin to age, the gap between men and women regarding their financial literacy widens. There may be a number of explanations for this, but the most likely is the fact that men tend to gain more first-hand experience with financial subjects than women, whether through their career or with their personal finances.

While proper financial education is lacking across the board for all individuals, first-hand experience serves as the best substitute to learn financial literacy. And, as the numbers show, men partake in these first-hand experiences at a much higher rate than women. According to a study from UBS, only 23% of women are in charge of their long-term finances globally. Further, about 56% of women under the age of thirty-four years old look to defer to their spouses for significant financial decisions. This is a rather concerning statistic, as only 52% of women older than fifty-one defer financial responsibilities (UBS). Such a trend indicates that younger generations of women are becoming less and less willing to take initiative with their finances, which may correlate with worsening financial literacy in younger women.

Without a proper grasp of financial literacy, it’s very likely for women to participate in detrimental financial behavior, which can make a mediocre financial situation much worse. Women with low financial literacy are five times more likely to have difficulties making ends meet, three times more likely to be debt constrained, and three times more likely to be able to withstand a $2,000 emergency (TIAA).

As mentioned earlier, this is particularly alarming because women already face a number of unique financial hardships. These financial burdens put women in a precarious position already. Being financially illiterate only ensures that women are unable to overcome these obstacles, which contributes to a widening wealth gap between genders.

Now, let’s take a look at some of these unique obstacles.

The Wage Gap

The most notable financial burden facing women is the wage gap. The gender wage gap is a hotly debated topic, as many claim the issue simply does not exist. Thus, before explaining this issue further, the misconceptions of the gender wage gap need to be outlined.

There is no arguing that a wage gap exists between genders, but the issue arises when discussing the reasoning behind this disparity. There are a number of factors that play into this phenomenon, such as work experience, field of employment, leave of absences, and blatant discrimination. However, the extent at which discrimination factors into this gap is contested. For example, overall, women make $0.83 for every dollar men make. However, when women are compared to men with the same position and qualifications, this gap decreases to $0.99 for every dollar a man makes (PayScale). What exactly does this indicate? Well, two things.

For one, this suggests that, with all things equal, discrimination may only account for a $0.01 gap instead of a $0.17 gap. While this is a much smaller gap than many advertise, it’s still troubling, as women doing the same exact job as a man with the same exact qualifications as a man are still paid less for no reason. This is just blatant gender discrimination.

Secondly, while the ‘controlled’ gap is only $0.01, we should not dismiss why women as a whole make $0.86 for every $1 a man makes. There is a phenomenon called occupational segregation, which is easily the culprit for the gender wage gap. Society dictates which careers are more appropriate for women as opposed to men. Women are likely encouraged to take on careers deemed more nurturing in nature, such as teaching or nursing. On the other hand, men are likely encouraged to pursue roles in higher-paying fields, like finance and STEM. Having this pre-conceived notion of certain jobs being appropriate for each gender is harmful. It’s just a glass ceiling that prevents women from realizing their true earning potential over the course of their career.

As just mentioned, men dominate higher-paying employment fields, which is a reason why women earn less overall in comparison. Over the lifetime of their careers, women earn $900,000 less than their male counterparts. When compared to men in a similar field with similar qualifications, women earn $80,000 less (PayScale). What does this mean for women? Because they are making less than men, women have to be even more careful with their financial habits. Having less capital, women have fewer opportunities to generate wealth and a very slim margin for error. And, because they are more likely to be financially illiterate, women are placed in a situation with the odds stacked against them.

So, while people want to continue to argue against the idea of a wage gap existing, there’s evidence to support just the opposite. Not only does the wage gap exist, but it perfectly captures the issues the women face when it comes to financial opportunities. And, this can also be seen in financial literacy. Gender norms prevent women from looking to partake in financial management within their relationships.

Women Live Longer

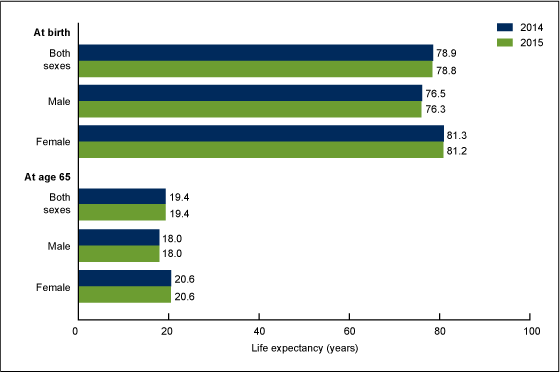

According to the Centers for Disease Control and Prevention, women have longer life expectancies than men on average. At birth, women have a life expectancy of 81.2 years old, while men have a life expectancy of 76.3. Women, on average, are expected to live five years, or over 6%, longer than men. While living longer definitely can be seen as a positive, it doesn’t come without its costs. Living is expensive, and the longer a person’s life is, the more expenses they will have to pay. Because women live longer, they will have more expenses in later stages of their life, especially in retirement. Consequently, women will have to play for longer retirements overall. As previously stated, women already earn less than men over their careers on average. Having fewer resources to save for retirement, women are at a disadvantage.

It should also be noted that if women outlive men, then many heterosexual women are going to be widows in their elder years. This could put further financial burden on women in multiple ways. For one, they no longer benefit from having an additional source of income from their partner. This could put additional stress, as the widow has to rely on a single income source to pay for expenses.

Second, women notably lack self-confidence when it comes to personal finances. Throughout their lives, many women defer financial obligations to their husbands. As noted before, UBS found that only 23% of women are in charge of their long-term finances globally. So, without having a partner with the experience of managing their finances, widowed women may also find difficulties in navigating their retirements.

To recap, heterosexual women are placed in a position where they need to plan a retirement where they don’t have to rely on their husband or male partner. If women across the board are less financially literate than men already, how could they prepare for retirements that last longer than those of men? It is important to reemphasize that women are earning less than men over the course of their careers already, which requires even more financial sophistication from women.

Women Have Shorter Careers

Another factor that plays a role in the gender wealth gap is career length due to maternity leave. From 1995 to 2015, the average month saw 273,000 women on maternity leave and only 13,000 men (American Public Health Association). Over a twenty-year period, the number of women taking maternity leave in any given month was twenty-one times greater than the amount of men. Thus, men actually have longer career tenure than women as a result.

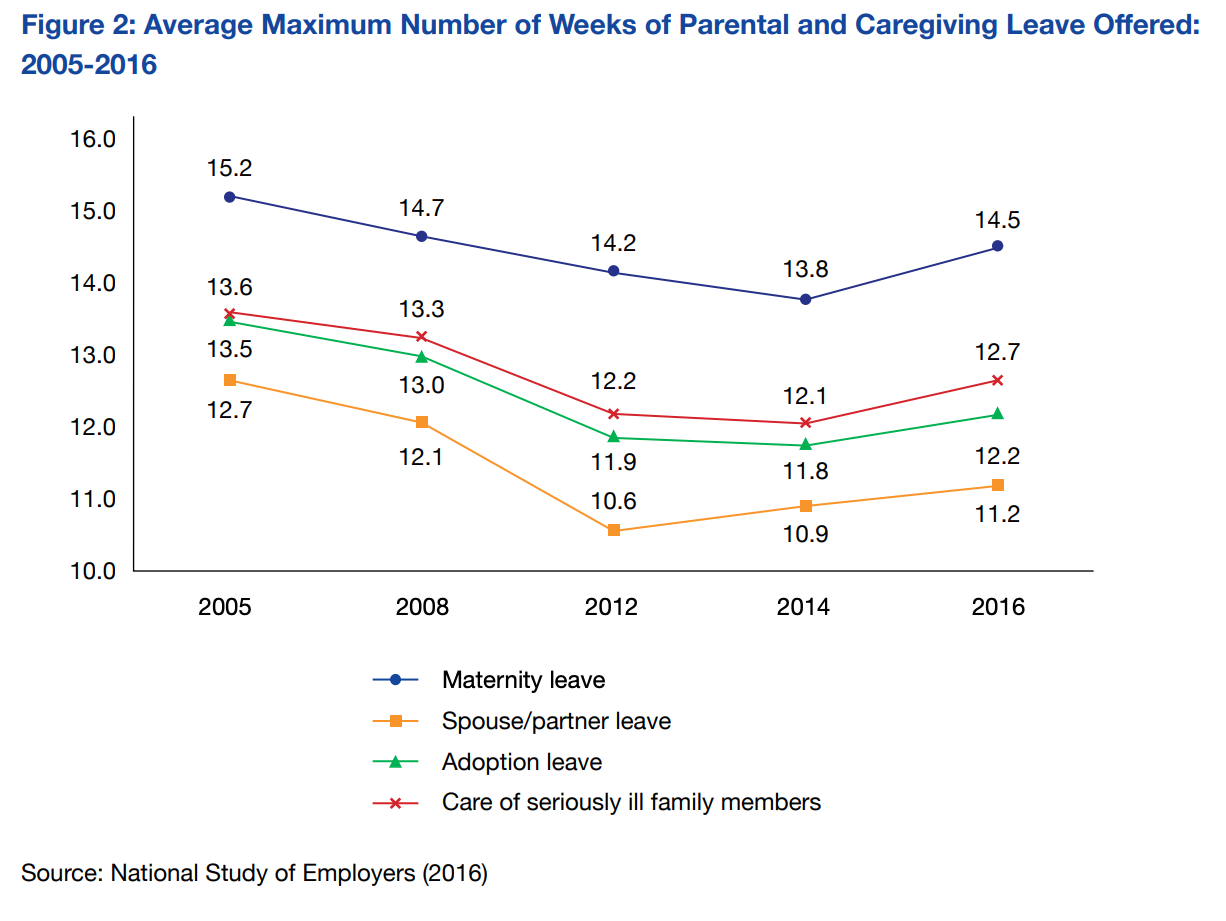

Maternity leave can last months, allowing male employees to get ahead in their careers and earn more. Unfortunately, many companies don’t have significant maternity leave benefits. According to the National Study of Employers, the average paid maternity leave was just over fourteen weeks in 2016, which is a decline from 2005. Additionally, only 51% of employees actually receive paid time off for maternity leave.

It is worth noting that women tend to have more than one child, which means multiple maternity leaves. As of 2020, women on average have about two children in the United States (Statista Research Department). Globally, women on average have two-and-a-half children (Our World in Data). With this information, it can be concluded that women on average take maternity leave about two to three times during their careers. This could result in women missing almost a full year of work during parts of their career where the most development is made.

According to the Pew Research Center, today, the average age at which women have children is twenty-six years old, which is an increase from twenty-three in 1994 (Pew Research Center). The average woman is having children at an older age now than in previous generations. There are definitely positive aspects to this change, as fewer children will be born into financial instability associated with women in their late teens and early twenties. However, this could also be troubling in regards to women’s careers. By having children at older stages of life, women are forced to take maternity leave in critical times of their career where they may have realized an increase in salary.

An additional negative effect of maternity leave is the impact it has on retirement benefits. Upon retirement, women receive benefits worth only two-thirds of those of men (Brookings Institute). This is a direct result of earning less throughout their careers. These retirement benefits reflect how much a worker makes over their career. Because women earn less, their retirement benefits are less. Facing a longer retirement, women also must overcome making less throughout their careers and receiving fewer benefits in retirement than their male counterparts. However, as mentioned in the previous chapter, women are financially illiterate at a higher rate than men, which only compounds the issues at play here. Because of the obstacles they face, women need financial literacy significantly more than men.

The Solution

As you may know, I am a big advocate of financial literacy, and this article clearly shows its importance in society. Financial literacy can provide tremendous financial opportunities to people, especially those in marginalized communities. However, a lack of financial literacy can have the exact opposite effect, further marginalizing these groups from seeing upward social mobility.

Across the board, financial education needs to be emphasized in society. There are number of ways that this can be done, including:

- Enacting effective school programs/curriculums

- Making conversations about finances less taboo

- Having financially literate individuals teach others

- Spreading awareness so people can self-educate (through platforms like this!)

A combination of these could definitely improve financial literacy, which is low among all genders, races, and even socioeconomic classes. While it is a widespread issue, promoting financial education would be specifically beneficial to women, who face unique challenges. And this could be seen as a time-pressed issue, as women have a once-in-a-generation opportunity over this decade to decrease the gender wealth gap.

By 2030, it is estimated that $59 trillion in wealth will be transferred from baby boomers to the next generation. Women are expected to inherit roughly 70% of wealth transferred this generation (Bankrate). Based on these statistics, women will have tremendous opportunities to achieve upward mobility to reach income equity and equality when compared to men. This could also create a change in dynamic of who manages spousal finances. With more wealth, women could assume a more significant role in managing finances than previously and their male counterparts.

However, with low financial literacy, it is unclear whether women will be prepared to handle this new influx of wealth. This would ultimately result in a squandered opportunity for many women in society at no fault of their own. Thus, it is imperative that financial literacy is taught to women to take advantage of such an opportunity.